Money is something that we all are familiar with but sometimes don’t know what to do with it? Mainly we have three options. Spending, saving and investing. Spending is the easiest way and it finds its way but other two options need knowledge, awareness and thorough analysis before choosing any one of these.

Money is something that we all are familiar with but sometimes don’t know what to do with it? Mainly we have three options. Spending, saving and investing. Spending is the easiest way and it finds its way but other two options need knowledge, awareness and thorough analysis before choosing any one of these.

Both savings and investment play a very important role in life to strengthen our financial position, but there are certain situations when one is better than the other. So, before we make any decision involving money, let us learn about saving and investment to take care of our hard earned money.

What is savings?

Traditionally, Savings is defined as the part of consumer’s disposable income which is not used for current consumption, i.e. whatever is left in the hands of a person, after paying all the expenses. So, it can be defined as difference of our earning and expenses.

EARNINGS – EXPENDITURE= SAVINGS

However, a smart investor always takes it other way i.e., Difference of Earning and Savings is expenditure.

EARNINGS – SAVINGS = EXPENDITURE.

So, savings should be the first priority as per the set benchmark and then whatever is left can be used as an outer benchmark for our expenditure. In other words, saving is simply money kept aside for future use. It’s a first step in building our wealth, which is decided by our level of income. The higher the income, the higher is his capacity to save.

So, savings should be the first priority as per the set benchmark and then whatever is left can be used as an outer benchmark for our expenditure. In other words, saving is simply money kept aside for future use. It’s a first step in building our wealth, which is decided by our level of income. The higher the income, the higher is his capacity to save.

Why savings?

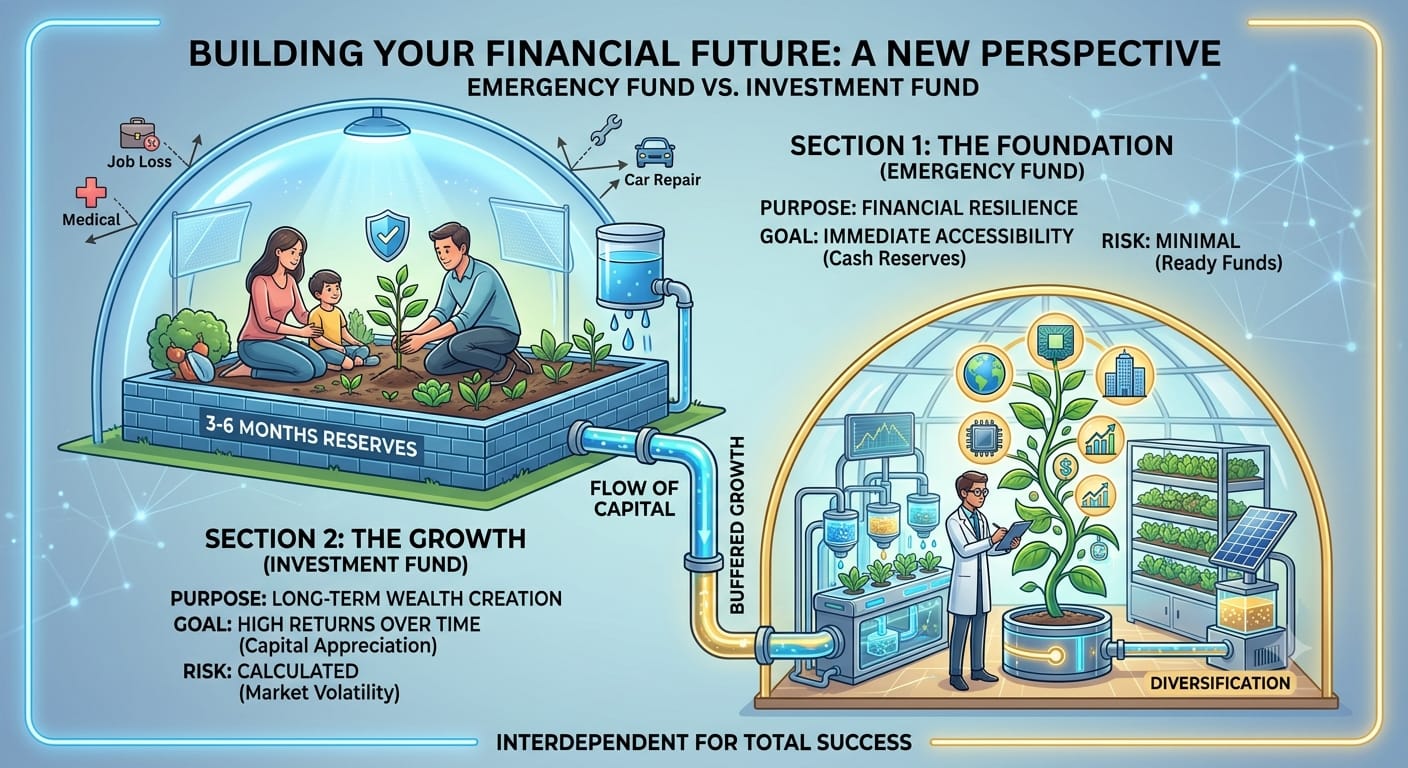

Purpose of saving money is to make it available when we need it. Savings makes a person financially strong and secure. We might need money for an emergency or in an urgent medical exigency .Everyone ought to have funds for taking care of at least six months’ living expenses, ‘just in case’ of loss of job and to meet unexpected situations. So, the credit crunch and impending recession are encouraging factors to save more.

If in near future, we are planning to purchase any asset like house or car; fund will be required for making down payment. If we want a long family holiday or expensive jewellery, we need to go for savings in advance.

In nutshell, if we want quick liquidity, then savings is a good option. Another purpose of savings is to generate investible income.

How to save?

There are several ways through which a person can save money like, accumulating it in the form of cash, depositing it in the Savings Account, Fixed Deposit, Pension account or in any investment fund. It can be easy to do – just go to your bank and open account with commitment to deposit money in it regularly. You can open Recurring Account with standing instructions from your Saving Accounts. Students can also open account. Digital FDs is a wonderful liquid fund as its payment is very easy. We can do with few clicks of mouse anywhere and anytime between 8.00 am to 8.00 pm.

There are several ways through which a person can save money like, accumulating it in the form of cash, depositing it in the Savings Account, Fixed Deposit, Pension account or in any investment fund. It can be easy to do – just go to your bank and open account with commitment to deposit money in it regularly. You can open Recurring Account with standing instructions from your Saving Accounts. Students can also open account. Digital FDs is a wonderful liquid fund as its payment is very easy. We can do with few clicks of mouse anywhere and anytime between 8.00 am to 8.00 pm.

Savings is the safer route because the amount in our bank account won’t typically decrease unless you withdraw funds, but interest rates on savings don’t allow our money to grow very quickly. Moreover, inflation rate may be higher than the Bank interest rates of savings account and even FDs. This means over time, your savings could lose purchasing power. This is the situation that tempts people to invest to receive higher returns and beat inflation.

It is important to track our savings, putting a deadline, or timeline, and a value to goals. Then we will be know how much we need and how much to save monthly.

What is investment?

Investing is the deliberate function of deploying income in a planned manner to reach a predetermined objective. Investment is the act of allocation of the saved money in the financial products, with intention of earning profits, which of course will come with some risks.

Why to invest?

As inflation goes up, it’ll chip away our money’s purchasing power, eroding purchasing power of our savings. Therefore, once we have a comfortable cushion of savings, we should also consider investing.

The ultimate purpose of investment is creation of wealth which can be in the form of appreciation in capital, interest earnings, dividend income, rental income etc. Investment can be made in different investment vehicles like stocks, PPF, bonds, mutual funds, commodities, options, currency, futures, index tracking fund or any other securities or assets.

How to invest?

There can be no investment without savings. If you don’t have an emergency fund, you have to work on saving first. If you already have an emergency fund including sustenance fund for at least six months, then you can go for Investment.

Investing is an art. It starts with asking and answering questions about future objectives e.g. what will be higher education expenses of my children? Is there any planning to buy any kind of movable/immovable property? If yes, When? What to do for the expenses of the children’s wedding? What is my post retirement planning? These questions can assist us in creating an investment plan.

The key to a successful investing career is long term planning. The longer we can invest, better it may be in terms of the better return. It is important to invest wisely.

Risk and returns are always interrelated. However, it is also true that we can reap more money with the same investment vehicle if we plan wisely.

Following options are available for investment:

- Government Schemes: If we want to go for safe, secure and long term with steady growth, we have to invest in schemes like Public Provident Fund (PPF), Senior Citizen Saving Scheme (SCSS) or Sukanya Samruddhi Yojna (SSY). Age and purpose are the key factors for these schemes.

- Bank FDs/MODs: We can go with Bank FD for some of our funds but not all, for steady and higher interest income with liquidity in comparison to savings account. Declining interest rates is a major concern here.

- Mutual Funds, gives a piece of a ready-made investment basket managed by experts with many options. It’s a good way to access different opportunities and markets which suits our risk appetite and goals. We can set up monthly investment and withdraw plans.

- Stocks, or securities, are amongst the top investment priorities of many people who want to grow their funds faster. With stocks we are buying a tiny slice of a company, so we may gain or lose money depending on the company’s financial performance. Dividends to shareholders are another benefit in this option. However, the stock market also carries higher risk. There is possibility that individual stocks where we invest may go completely bust, leaving you with nothing. So, it is advisable to have diversified portfolio .

- Government bonds are another option; these can have long terms and low rates of return. They mitigate the risk and provide excellent safety. But we need comparatively higher amount to invest.

- Life Insurance Policies provide protection with financial help the nominee of the insured in case of unfortunate event. Also, policies may be useful as a pension plan option in old age in case of endowment plan with reasonably good returns.

- Other investment options like gold, silver, real estate other long term assets in physical as well as in Demat form.

- Option / Money Market can be used to make money faster, but risks associated are also very high.

There are different ways to measure how profitable your investments are. The general principle is to look at the cost of anything you purchased compared to the current price. Keeping decent records of prices and returns is important to know that you are making the right decisions.

Key Differences between Savings and Investment

A general thumb rule is that savings should be for short term while investment should be for long term. It’s important to understand the basic differences between savings and investment, which are explained in the following table:

| BASIS FOR COMPARISON | SAVINGS | INVESTMENT |

| Meaning | Savings denote that part of the person’s income which is not used for consumption. | Investment refers to investing funds in capital assets, with a view to generate returns. |

| Purpose | Savings are made to fulfill urgent requirements or for short term goal. | Investment is done to get higher returns for capital enhancement. |

| Risk | Low or negligible | High or Very high |

| Returns | Low or Negligible (It may be negative considering Inflation) | Comparatively high according to risk |

| Liquidity | High | Low |

In nutshell, if we have short-term goals and want to ensure safety of the fund, we can go for savings, if we have long term goals and have risk appetite; investment provides a better opportunity to get higher returns. Of course, ideally we should have a mix bucket.

Himanshu K Modi

Chief Manager (Faculty), SBILD, Bhavnagar.